Introduction

You’ve seen the advertisements and the flashy offers: earn cashback on every purchase, get free flights with travel miles, unlock exclusive perks. Credit card rewards are constantly marketed as a way to get something for nothing. For a university student on a tight budget, the allure is powerful. But are these programs truly beneficial, or are they a trap designed to encourage overspending and debt? The answer is: it depends entirely on you.

For the financially disciplined student, credit card rewards can be a fantastic tool to generate real value from everyday spending. For those who are not, they can be a dangerous path to high-interest debt. This article is a guide for the responsible student who is ready to move beyond simply avoiding debt and start making their money work for them. We will explore how to choose the right rewards card, how to maximize your earnings without overspending, and why the single most important rule is to avoid the high interest rate at all costs.

The Golden Rule: Pay Your Balance in Full, Always

Before we discuss any type of reward, one rule must be established as non-negotiable: you must pay your credit card balance in full, on time, every single month. If you cannot commit to this, the world of rewards cards is not for you, and that’s perfectly okay.

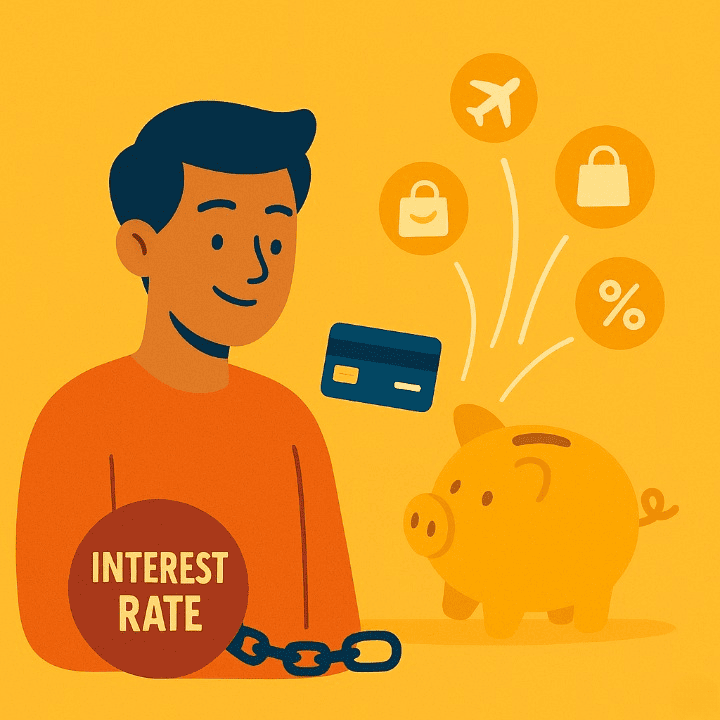

Here’s the simple math: a typical rewards credit card might offer 1.5% cashback on your purchases. However, that same card will likely have an interest rate of 20% or higher. If you carry a balance of just $500 for a year, you could pay over $100 in interest charges. That high interest rate will wipe out any small rewards you’ve earned and then some. Rewards are only a benefit when they are truly free; they are never worth paying interest for.

Understanding the Types of Rewards

Not all rewards programs are created equal. They generally fall into three main categories, each suited to different types of spenders.

- Cash Back: This is the simplest and most flexible type of reward. You earn a percentage of your spending back as cash, which can be redeemed as a statement credit, a direct deposit, or a check. For most students, a straightforward cashback card is the best place to start.

- Points: These are part of a flexible currency system. You earn points on your purchases, which can then be redeemed for a variety of things, including travel, gift cards, or merchandise through the bank’s own portal. They can sometimes offer a higher value than cashback if redeemed wisely, but they require more management.

- Travel Miles: These rewards are typically co-branded with a specific airline or hotel chain. You earn miles for every dollar you spend, which can be redeemed for flights or hotel stays. These cards are best for students who travel frequently and are loyal to a particular brand.

Choosing Your First Rewards Card: What to Look For

As a student, you should look for a card that fits your specific lifestyle and financial situation. Here are the key factors to consider:

- No Annual Fee: For your first rewards card, a “no annual fee” option is almost always the best choice. You want to earn value, not pay a yearly fee for the privilege of using the card.

- Relevant Bonus Categories: Many cards offer a higher reward rate (e.g., 3% or 5%) on specific spending categories. Look for a card that rewards you for how you already spend your money, such as on groceries, dining out, gas, or streaming services.

- Achievable Sign-Up Bonus: Many cards offer a large bonus (e.g., $200 cashback) if you spend a certain amount in the first few months. Only consider this if the spending requirement is something you can meet comfortably with your normal, budgeted expenses.

Beyond Points: The Hidden Power of Credit Card Insurance

One of the most overlooked benefits of many rewards cards, especially those geared toward travel, is the suite of built-in insurance perks. These can provide a significant financial safety net and are a valuable part of the card’s total offering. Common types of credit card insurance include:

- Trip Cancellation/Interruption Insurance: If your trip is canceled or cut short for a covered reason, this can reimburse you for your non-refundable travel expenses.

- Rental Car Insurance (Collision Damage Waiver): This allows you to decline the expensive insurance offered at the rental car counter, as your card provides coverage.

- Extended Warranty Protection: This automatically extends the manufacturer’s warranty on eligible items you purchase with your card.

These insurance benefits can save you hundreds of dollars and provide peace of mind, adding a layer of value far beyond simple cashback.

Rewards and Your Financial Health

When used correctly, a rewards credit card is more than just a payment tool; it’s a component of a healthy financial life.

- Building Excellent Credit: Using the card for regular purchases and paying it off in full every month is one of the most powerful ways to build an excellent credit history. This demonstrates to lenders that you are a responsible borrower.

- Financing Your Goals: The rewards you earn can become a small but meaningful part of your budget. The cashback you accumulate over a year could be a form of self-financing for your textbooks, a weekend trip to de-stress, or a contribution to your savings goals.

- Improving Well-being: The rewards can directly contribute to your health. Cashback can be used to subsidize a gym membership or buy healthier groceries. Travel points can be used for a much-needed break, which is a great investment in your mental health.

Conclusion

Credit card rewards programs offer a tantalizing proposition for students. They can be a fantastic way to generate value from your everyday spending, but they must be approached with discipline and a clear understanding of the risks. The power of rewards is completely negated by the destructive force of a high interest rate. The golden rule is, and will always be, to pay your balance in full.

By choosing the right card for your spending habits, using it only for budgeted expenses, and taking full advantage of hidden perks like travel insurance, you can transform your credit card from a simple payment method into a strategic financial tool. This responsible approach will not only earn you rewards but will also help you build an excellent credit history, setting the stage for a secure and prosperous financial future.