Introduction

You’ve seen it at the checkout of your favorite online stores: that tempting offer to split your purchase into four easy, interest-free payments. Services like Klarna, Afterpay, and Affirm, known as “Buy Now, Pay Later” (BNPL), have exploded in popularity, especially among young consumers. They offer a seemingly frictionless way to get what you want now without paying the full price upfront. But as this new form of financing becomes more integrated into our shopping habits, critical questions arise: How do these services really work? Are they truly a “smarter” way to pay? And most importantly, how do they impact your financial health and your credit score?

This article is your essential guide to navigating the world of Buy Now, Pay Later. We will deconstruct the business model, compare BNPL services head-to-head with a traditional credit card, and uncover the hidden risks that can affect your financial future. Understanding this tool is crucial for any student looking to make smart financial decisions in the modern digital economy.

How BNPL Works: The Illusion of ‘Free’ Financing

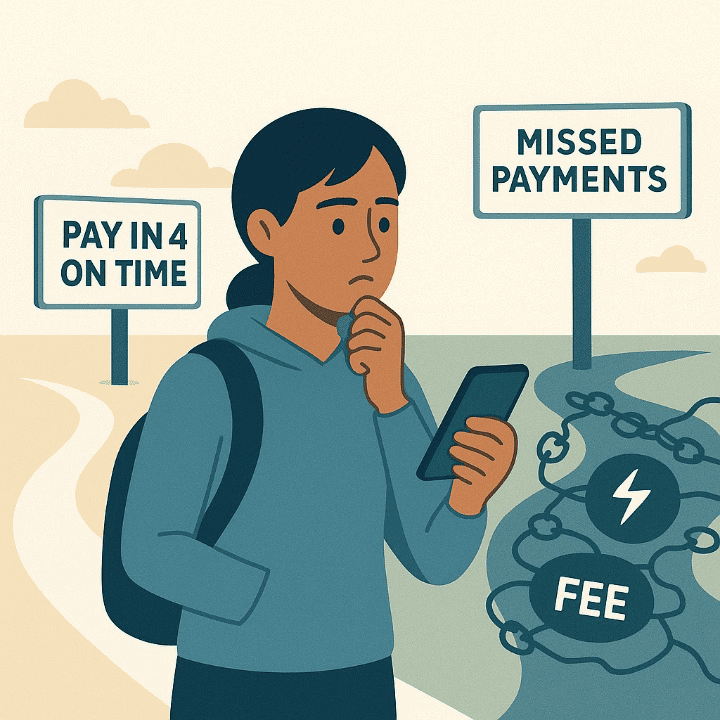

The primary appeal of BNPL is its simplicity and the promise of “interest-free” payments. The most common model is the “Pay-in-4,” where your total purchase is split into four equal installments, paid every two weeks. The first payment is made at the time of purchase, and the remaining three are automatically charged to your linked debit or credit card. For these short-term plans, if you make all your payments on time, you typically pay no interest or fees.

However, many BNPL providers also offer longer-term installment plans for larger purchases, which often function more like traditional loans. These longer-term financing plans frequently do come with an interest rate, which can sometimes be quite high. The “interest-free” marketing is powerful, but it’s crucial to understand that this promise is entirely conditional on your ability to pay on time. A single missed payment can result in hefty late fees, immediately erasing any perceived benefit.

BNPL vs. Credit Card: A Head-to-Head Comparison

Is using BNPL better than using a credit card? The answer is complex, as each has distinct advantages and disadvantages.

- Ease of Approval: BNPL services often use a “soft” credit check, which doesn’t affect your credit score. This makes them much easier to get approved for than a traditional credit card, especially for students with a limited credit history.

- Interest Costs: For short-term “Pay-in-4” plans, BNPL is the clear winner if you pay on time, as it’s genuinely interest-free. A credit card, in contrast, will charge a very high interest rate if you carry a balance past the due date.

- Building Credit: This is a crucial difference. Historically, most BNPL services did not report your payment history to the major credit bureaus. This meant that even if you used them responsibly, it did nothing to help you build a positive credit score. This is slowly changing, with some providers beginning to report payments. A traditional credit card, on the other hand, is one of the most reliable and powerful tools for building a strong credit history when used responsibly.

- Rewards and Protections: A credit card often comes with valuable rewards (like cashback) and consumer protections, such as fraud liability and purchase protection insurance. Most BNPL services offer minimal perks and fewer protections if there is a dispute with the merchant.

The Hidden Danger: How BNPL Can Hurt Your Credit Score

While BNPL can seem like a low-risk option, it can negatively impact your credit in several ways:

- Late Payments: If your BNPL provider does report to the credit bureaus, a single missed payment can be reported as a delinquency, damaging your credit score just like a late credit card payment would.

- Debt Collections: If you fail to pay your BNPL debt, the provider can send your account to a debt collection agency. A collection account on your credit report is a major negative event and will severely harm your score for years.

- Hard Inquiries: While most “Pay-in-4” plans use a soft check, applying for some of the longer-term BNPL financing plans can result in a hard credit inquiry, which can cause a small, temporary dip in your credit score.

The Psychological Trap: Overspending and Your Mental Health

Perhaps the greatest risk of BNPL is psychological. Because it breaks down a large purchase into smaller, more manageable-looking payments, it can trick your brain into thinking you can afford more than you actually can. This friction-free process makes it incredibly easy to overspend and accumulate multiple small debts from different retailers simultaneously—a phenomenon known as “debt stacking.”

Keeping track of multiple payment schedules can become overwhelming. The financial stress and anxiety that come from falling behind on these payments can have a serious negative impact on a student’s mental health, affecting their ability to focus on their studies and well-being.

A Smart Student’s Rulebook for Using BNPL

If you choose to use BNPL services, you must do so with a strict set of rules to protect yourself.

- Rule 1: Use It for Budgeted Purchases Only. Never use BNPL as a way to buy something you couldn’t afford to pay for in full with your own money today. Treat it as a cash flow tool, not an extension of your budget.

- Rule 2: Automate Your Payments. Always link your BNPL plan to a reliable debit card or bank account that you know will have sufficient funds. This is the best way to avoid accidental late payments.

- Rule 3: Track Your Plans Diligently. Use a budgeting app, a spreadsheet, or a simple notebook to keep a running list of all your ongoing BNPL plans, their amounts, and their due dates.

- Rule 4: Read the Fine Print. Before you click “confirm,” understand the late fee structure and the interest rate, if any, associated with the plan.

Conclusion

Buy Now, Pay Later services are a powerful and convenient new tool in the world of personal financing, but they are not a risk-free replacement for traditional payment methods. They are a form of credit and must be treated with the same discipline and respect as a credit card or a loan. By understanding the terms, comparing the pros and cons, and using these services strictly for planned and budgeted purchases, students can enjoy the convenience without falling into a dangerous debt trap.

Ultimately, responsible use is the key. Your diligence is what protects your budget, your long-term credit score, and your overall financial health in this new and evolving era of digital payments.